Q1 2026 MARKET RECAP AND OUTLOOK

Entering 2026, the global financial picture was decidedly mixed, as investors weighed concerns about valuations, consumer sentiment and ongoing sources of volatility (think tariffs/trade deals and U.S. mid-term elections), versus resilient corporate earnings, AI productivity gains, and optimism around expected interest rate cuts. Markets in the early part of the quarter were largely positive, aside from some sector-specific selloffs in companies perceived as vulnerable to AI disruption (the so-called “AI loser trade”), but it was the U.S. and Israel attack on Iran in late February that ended up dominating the quarter.

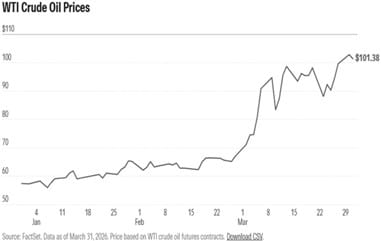

Oil prices surged to near record highs, stock and bond markets fell, and investors were forced to grapple with a new level of uncertainty around economic growth, inflation, and the path of interest rates, moving forward. By quarter’s end, most stock markets had been pulled into negative territory for the year.

While the broad U.S. indices were all substantially down for the quarter (S&P 500 Index -4.6% / NASDAQ Composite Index -7.0% / Dow Jones Industrial Average -3.2%), it was far from a sea of red, as investors rotated into undervalued stocks and more defensive areas of the markets. Surprisingly, only five of the eleven S&P 500 sectors posted negative returns, led by financials (-9.4%), consumer discretionary (-9.2%) and technology (-9.1%). Unsurprisingly, surging oil prices led to energy (+38.3%) being the best performing sector, followed by materials (+9.7%) and utilities (+8.3%). To complete the rotation from recent trends, value outperformed growth, small and mid caps outperformed large caps and dividend payers outperformed non-dividend payers.

Canada was a bright spot globally, with the S&P/TSX Composite Index up +3.9% in Q1, largely a result of our resource-centric economy. The energy (+30.1%) and materials sectors (+10.7%) dominated the quarter, although only five of the eleven sectors were positive. Information technology (- 22.5%) was the poorest performer, followed by health care (-4.5%) and real estate (-4.3%). Similar to the U.S., investors’ shifting preferences for dividend payers and defensive stocks were a boost to Canadian markets during the quarter.

International markets were largely negative last quarter, with the U.K. (+4.1%, boosted by a relatively large energy sector weighting) and Japan (+3.0%, supported by new pro-growth government) being two of the only bright spots. Most of the Eurozone (-2.3%) struggled, due to a high reliance on imported energy and a cyclical industrial base. Emerging markets were mixed, with strength in technology-focused markets like Korea (+24.1%), but sharply down in China (-8.5%, dragged lower by the AI loser trade) and India (-13.6%, based on growth concerns and reliance on imported oil).

While fixed income indices had a relatively benign quarter, with the FTSE Canada Bond Universe up +0.2% and the Morningstar Global Core Bond Index up +1.0%, there was much more going on below the surface. Bond yields jumped as the oil price shock renewed inflation concerns. According to Morningstar Research, “the forecasts for rate cuts have largely vanished, and bond traders are tilting toward the possibility of a rate hike.” This led to declines in the more interest rate sensitive parts of the fixed income market (think long-term bonds) and increases to things like mortgage and line of credit rates, further stressing already cash-strapped consumers.

One of the more noteworthy items in Q1 was the volatility in gold. After its unprecedented rally in 2025, gold climbed 25% further to start the year, only to unexpectedly plunge more than 13% at the end of January (one of the most violent selloffs in modern precious metals history, and still largely unexplained). Furthermore, despite having a reputation as a safe haven and a store of value amid inflation, gold prices have fallen further since the onset of the war in Iran.

As we head into the second quarter, the outlook is murky and highly dependent on the outcomes of on-again/off-again Iran war ceasefire negations. Until a more permanent end to hostilities is reached, we expect markets will be volatile and highly reactive to news headlines.

OUTLOOK – Anything but “Strait” forward

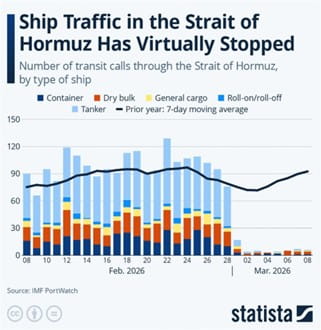

Heading into 2026, few investors would have had the Strait of Hormuz listed among their key investment risks to start the year. AI, valuations, inflation, tariffs, consumer sentiment…yes, but a narrow channel of water half a world away? Not likely even in the top 10. Tension between Iran and the Western countries is nothing new, but a near complete closure of the Strait of Hormuz was considered an unlikely tail risk, the lasting impacts of which have potentially been underestimated by markets (and a development that will likely force a reassessment of trade routes, energy supply chains, and potentially, infrastructure spending).

The Strait of Hormuz has long been known as a strategically important chokepoint, with 20% of the world’s liquefied natural gas and 25% of seaborne oil passing through these waters. While most is destined for Asia, it is also a major source for Europe. However, as a global commodity, oil prices have skyrocketed across the globe, with oil now 60-80% more expensive than it was at the beginning of 2026, leading to increased gasoline prices and surcharges for things like air travel and shipping (both Canada Post and Amazon have recently added fuel surcharges).

According to Justin Truong, Director of Investment Strategy at Mackenzie Investments, “The market is beginning to move beyond the initial oil-shock playbook. What started as a flow crisis looked painful but manageable if it lasted only days. Four weeks into the war, that risk has evolved into a more tangible and potentially longer-lasting supply shock, with disrupted Gulf flows and attacks on energy infrastructure making the shock harder to dismiss as temporary. That helps explain why the market’s focus is broadening from oil itself to the second-order effects: higher inflation expectations, rising interest rates, tighter financial conditions, and growing doubts about how quickly policymakers can respond.”

Investors are used to geopolitical events following a familiar script — typically, the initial sell-off is followed by a period of uncertainty, some resolution, and an eventual recovery. What makes the Strait of Hormuz unique is not the conflict itself, but the importance of what flows through it:

- Fertilizer: the conflict has restricted about 30% of global urea trade (the most widely traded fertilizer, which helps plants grow and boosts yields). This has led to shortages and skyrocketing prices because of shipping delays and the soaring price of liquefied natural gas — an essential ingredient. This threatens to reduce crop yields and exacerbate global food insecurity.

- Aluminium: Gulf countries, which supply nearly 10% of the world’s aluminium, are facing export This threatens to delay production for the construction, vehicle, and machinery industries.

- Helium: The closure of shipping routes, particularly from Qatar, is causing a tightening in the global helium This is beginning to impact critical manufacturing sectors, including semiconductor manufacturing, fibre optics, and medical device cooling.

- Petrochemicals: The reduction in energy supply is impacting the production of petrochemicals, leading to increased costs for packaging and materials.

What markets may be underestimating is the potential inflationary impact of these less obvious, second-order effects. Combine this with rising bond yields (which directly impact mortgage and line of credit rates), and consumers just starting to feel some relief from the inflation of the last few years could see this trend re-ignite. The longer this conflict persists, the greater the risk that impacts are felt in the real economy through weaker spending, softer hiring, tighter margins, and reduction in corporate earnings…areas that so far have remained resilient.

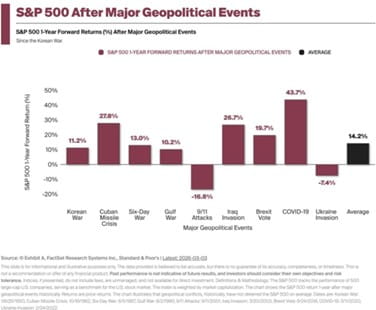

Until marine traffic is again moving freely through the Strait of Hormuz, concerns over energy prices and emerging shortages of the above-noted items will weigh on markets, so we expect volatility to persist. In these times, it is important that investors stick to their plan and stay diversified. As shown in the chart to the right, markets historically have found their footing after major geopolitical events.

We build out portfolios to withstand these types of events. Diversification of sectors, investment styles, income streams, and asset classes puts us in the best position to safeguard capital and navigate whatever comes next. And as always, we are here to answer any of your questions, so please do not hesitate to reach out.

Ryan Cramp, CIM, CFP®

Portfolio Manager

Private Client Group, Raymond James Ltd.

Michael Higgins, BCom, CIM®, FCSI

Associate Portfolio Manager

Private Client Group, Raymond James Ltd.

This Quarterly Market Commentary has been prepared by Ryan Cramp and Michael Higgins and expresses the opinions of the authors and not necessarily those of Raymond James Ltd. (RJL). Statistics and factual data and other information are from sources RJL believes to be reliable but their accuracy cannot be guaranteed. The client account performance may vary from the model portfolio due to several factors, including the timing of contributions and dates invested in the model. The performance reported is that of the account that represents the model, not a composite. Performance calculation for the models may be different than the index used as a reference point. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. This Quarterly Market Commentary is intended for distribution only in those jurisdictions where RJL and the author are registered. Securities-related products and services are offered through Raymond James Ltd., member-Canadian Investor Protection Fund.